A Decade of Hot Springs: First-Ever Ten-Year Time

Series Data

There is no question that nature is essential to all dimensions of our wellness. Nature is also an essential “ingredient” to all kinds of experiences, services and products across the wellness economy: from biophilic design, to forest bathing, to seaweed wraps and plant-based supplements, and so much more. In honor of Earth Day, our data feature for April focuses on what is arguably the most nature-rooted sector in the entire wellness economy: thermal and mineral springs. GWI’s research team has been compiling global data on the thermal/mineral springs sector since 2013. Here, we provide the first-ever snapshot of our full time-series dataset for 2013-2022, and projecting forward to 2027.

How do we collect thermal/mineral springs data?

Users of GWI’s wellness economy data may not realize that we use a very granular, “bottom-up” approach for measuring the thermal/mineral springs market. There is no econometric model that can be used to estimate this sector, because every country’s thermal/mineral springs market is based on its own unique set of geothermal/natural resources and historical/cultural factors that shape how spring waters have been used and developed over time.

Since 2013, GWI’s research team has compiled a massive database containing listings for 6,500 thermal/mineral springs establishments, located in 130 countries all over the world. While we can never be sure that our database is 100% exhaustive (every year we learn about a few smaller springs properties that we had previously “missed”!), we are confident that the thoroughness of our database provides a strong basis for making accurate estimates of the industry’s size in each country. There are about 16 countries (including China, Japan, Germany, and many other European countries) where we have alternative data sources, or where the thermal/mineral springs industry is too large for us to count properties. In these cases, we rely upon government and industry association datasets in order to compile our estimates.

For over a decade, our research effort has also benefitted immensely from the deep global experience and insights of members of GWI’s very active Hot Springs Initiative. Initiative members have supported our work in many ways, including conducting industry surveys, helping us to access foreign language government datasets for hot springs, and even sharing revenue information for their own businesses.

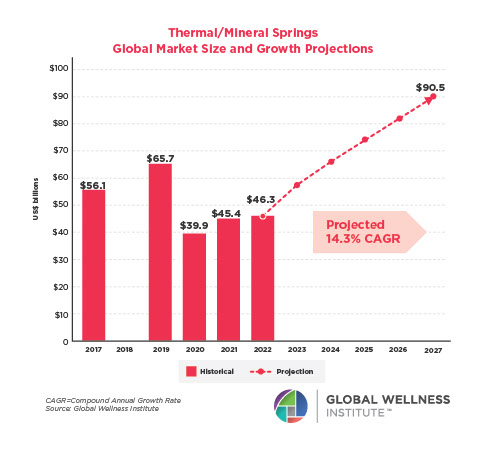

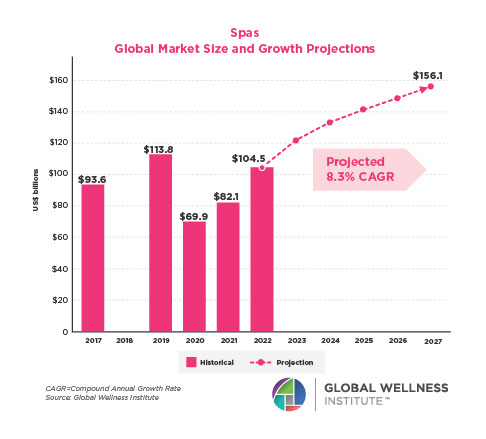

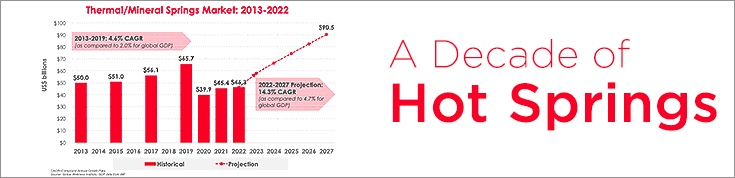

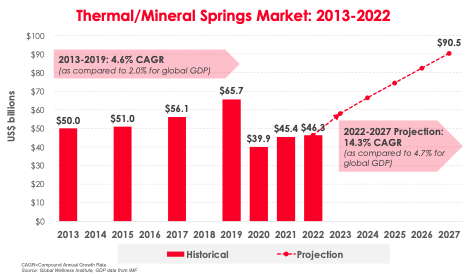

The thermal/mineral springs sector was hit hard by the pandemic, but its longer-term growth trajectory is robust.

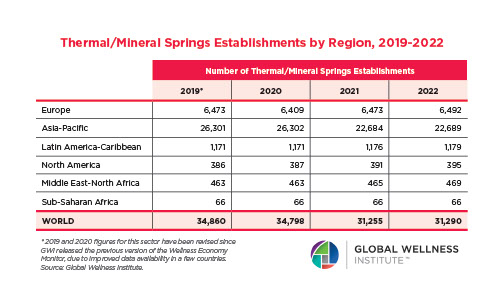

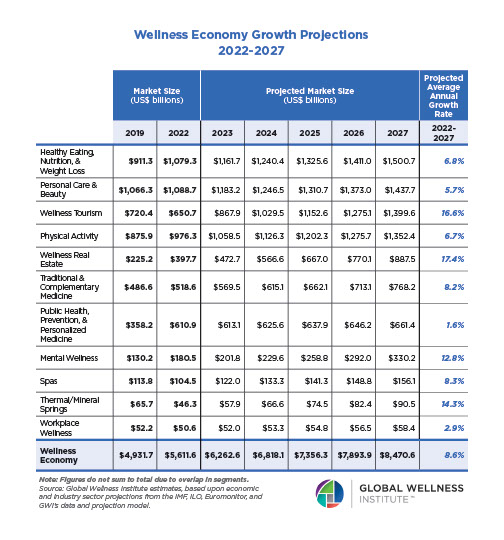

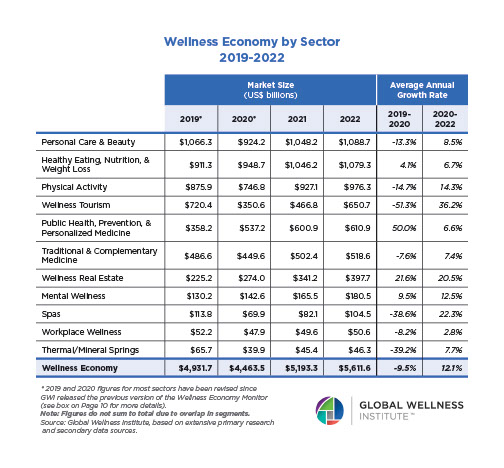

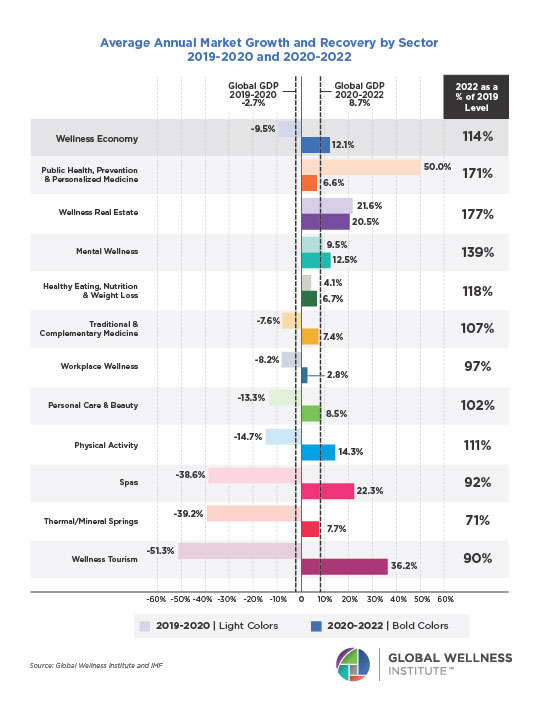

We estimate there were 31,290 thermal/mineral springs establishments operating in 130 countries in 2022. Prior to the pandemic, thermal/mineral springs revenues were growing at a robust rate of 4.6% annually (2013-2019), which is more than double the rate of global GDP growth during this time period. Because springs are largely tourism-dependent businesses, the sector took a strong hit from the border closures, travel bans, business shutdowns, and capacity restrictions during the pandemic. The market fell by 39% globally in 2020, and business revenues have slowly come back in 2021 and 2022 (but are still well below their pre-pandemic peak of $65.7 billion). At the end of 2022, springs businesses across most of the world were at 75-90% of their pre-pandemic level, except for China and Japan (48-60% of their pre-pandemic level).

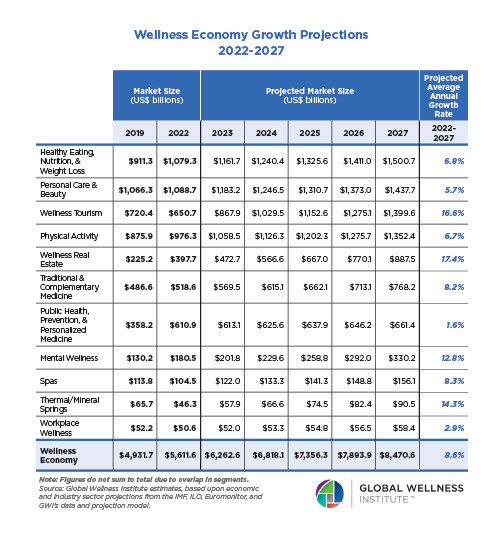

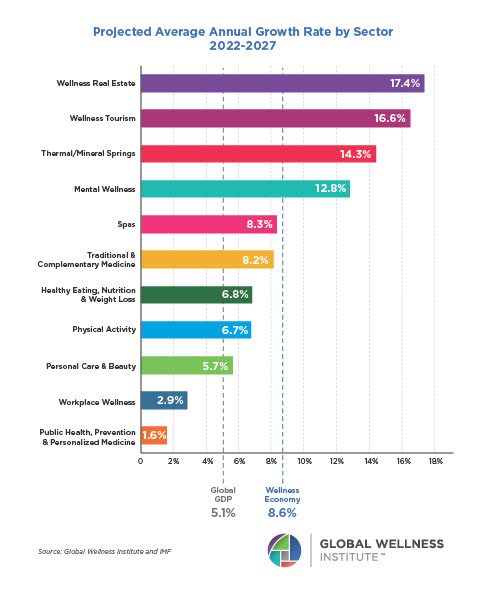

GWI’s future projection for thermal/mineral springs market growth accounts for a few years of post-pandemic recovery, underpinned by ongoing strong growth trends driven by rising consumer demand for these kinds of experiences. With a projected annual growth rate of 14.3% from 2022 to 2027, we expect that the springs sector will fully recover and exceed its pre-pandemic level by 2024. Note that these projections were made in the fall of 2023, and they will be updated with the release of the next Global Wellness Economy Monitor in fall 2024.

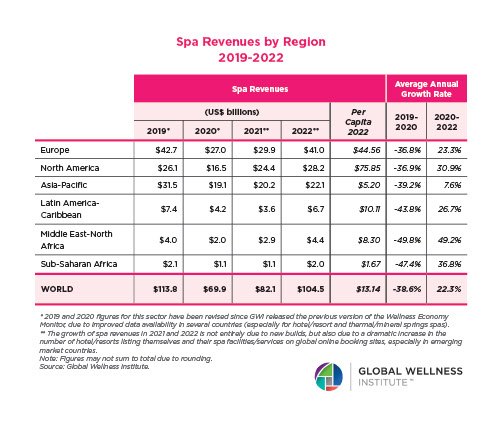

Unbundling growth trends at the regional level.

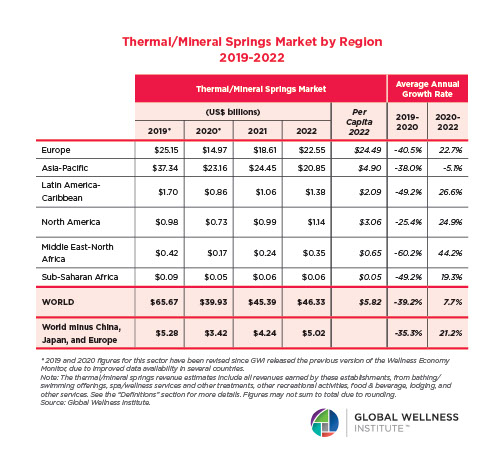

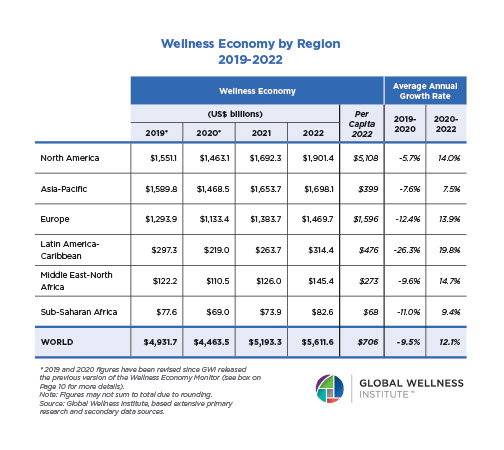

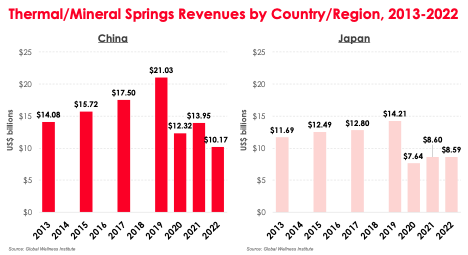

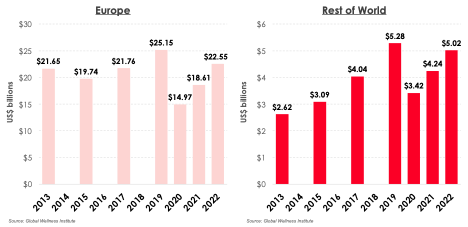

The thermal/mineral springs sector is heavily concentrated in Asia-Pacific and Europe, reflecting the centuries-old history of water-based healing and relaxation in these two regions. Together, Asia-Pacific and Europe account for 94% of revenues and 93% of establishments in this sector (2022 data). Because these regions are so large, the global growth rate is dominated by them, masking interesting developments in other smaller country markets. Here, we unbundle the market data across China, Japan, Europe, and the rest of the world, to explore the pandemic impacts and growth trends across these diverse regions.

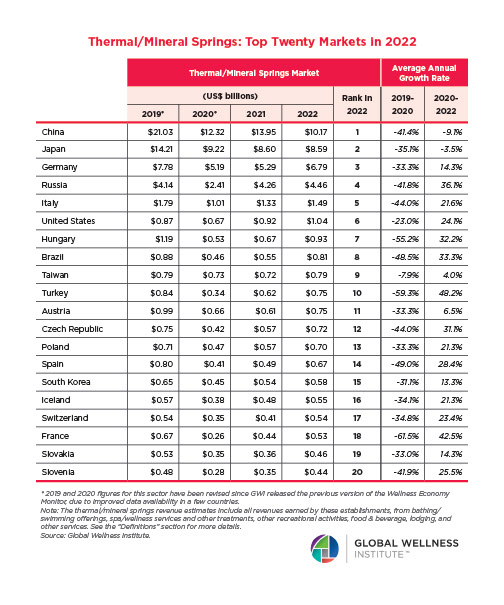

- China and Japan: China and Japan together account for 40% of global revenues and 68% of all establishments (2022 data), although their share of the global market has declined quite a bit with the prolonged downturn of the sector in both countries throughout 2021 and 2022. Japan alone, with its estimated 17,257 onsen, is home to 55% of all thermal/mineral springs establishments in the world. In China, the prolonged pandemic, alongside weakening economic conditions, meant that thermal springs revenues continued to plummet through 2022, even as businesses across the rest of the world were recovering. Japan’s large hot springs sector has seen the closure of about 3,500 onsen (primarily day-visit establishments) in recent years, although this trend has been driven by many factors beyond just the pandemic, and industry revenues have continued to grow in Yen terms over the last two years (currency depreciation reduced the sector’s size in 2022 when expressed in US dollar terms).

- Europe: Central, Southern and Eastern Europe have a massive industry of historic thermal/mineral springs-based health resorts and sanatoria. Europe accounted for 49% of all global revenues in this sector in 2022. In the early stages of the pandemic, businesses across many countries lost a substantial portion of their customer base when Russian tourism stopped after the invasion of Ukraine. Many European hot springs businesses have also been struggling in recent years due to high energy prices and post-pandemic staffing shortages. Despite these challenges, the sector’s revenues have been rapidly recovering in 2021 and 2022, with 23% average annual growth from 2020 to 2022. Europe’s springs sector is likely to recover to its pre-pandemic level as of 2023. One important note about the time-series data for Europe is that currency depreciation against the US dollar in both 2015 and 2022 has dampened the region’s size and growth rate in those years when measured in US dollars; the growth rates in both years would be higher if expressed in Euros.

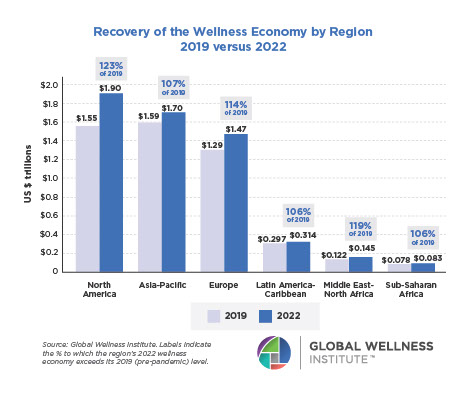

- Rest of the World: The post-pandemic picture for the springs sector has been far less gloomy in the rest of the world. Across North America, the rest of Asia-Pacific, and Latin-America, the hot springs sector has grown at a robust 21.2% annually since 2020, and business has nearly returned to pre-pandemic levels. In some markets where the COVID-19 outbreak was less severe (e.g., Taiwan), and in regions where lockdown measures were less strict, some establishments saw only minor/temporary downturns in customer visits, and some have even experienced strong growth throughout the pandemic. For example, in parts of the western United States, Australia, and New Zealand, some establishments have reported growth of 10-20% or more in recent years, as customers flocked to bathing as a “COVID-safe” outdoor activity and as domestic tourists and residents filled the slots left by international visitors. In Australia, New Zealand and the United States hot springs businesses had a record-setting year in 2022, with revenues far exceeding their pre-pandemic levels.

The future of the thermal/mineral springs market is strong.

Prior to the pandemic, thermal/mineral springs was one of the fastest-growing sectors in the wellness economy. GWI predicts ongoing steady and strong growth in the coming years, building on the rapidly growing consumer, business, and government interest in hot springs and water-based experiences of all types. Thermal/mineral springs bathing experiences appeal to an expanding segment of consumers who are seeking to connect with nature, experience cultural traditions, and pursue alternative modalities for healing, rehabilitation and prevention. Many consumers from places that do not have the tradition of water treatments or public bathing are “discovering” the therapeutic benefits of thermal waters, saunas, and cold plunges when they visit spas and springs, or when they travel. The strong future for the springs sector is evident in the high level of investment and development sustained throughout the pandemic and in the future pipeline. We estimate that at least 150 new thermal/mineral springs establishments opened from 2020 to 2022, across every region of the world, and over 250 projects are in the pipeline for future new openings/development.

For more data on the thermal/mineral springs sector, see the most recent edition of GWI’s Global Wellness Economy Monitor.