Wellness Communities and Real Estate Initiative

2026 Trends

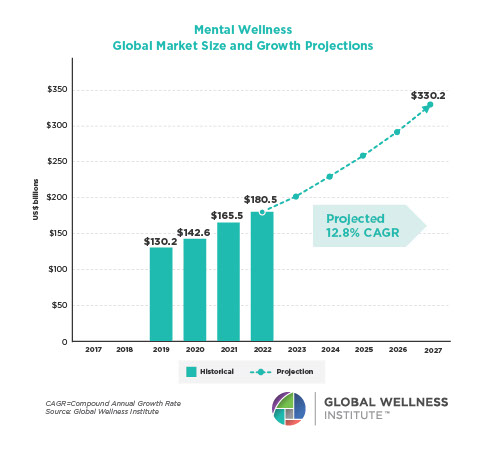

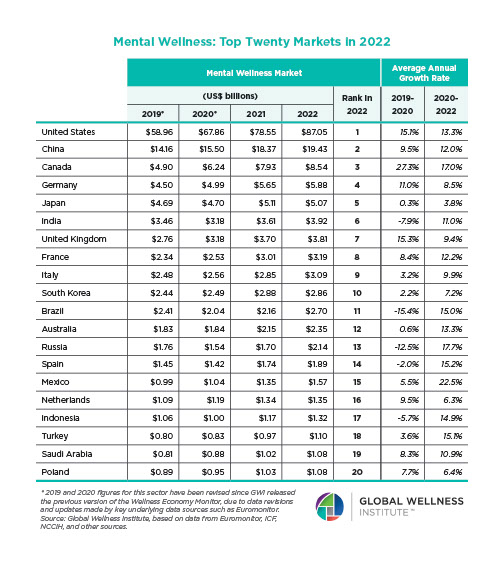

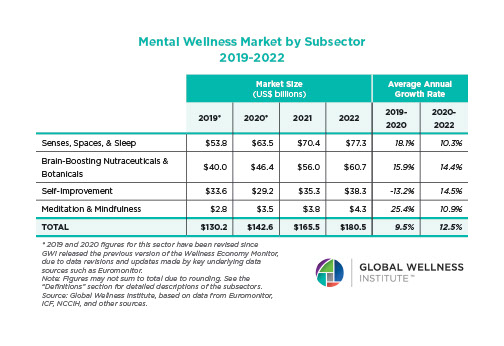

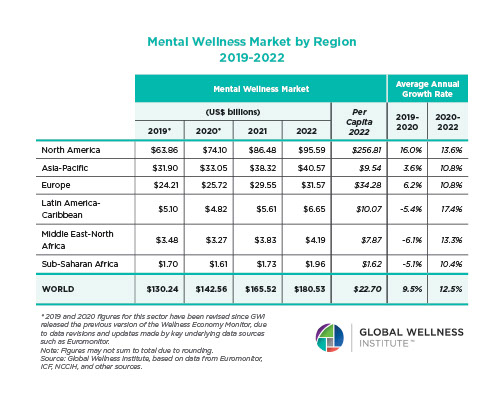

![]()

Initiative Chair: Teri Slavik-Tsuyuki, Principal, tst ink LLC, United States

Initiative Vice-Chair: Jean-François Garneau, Chief Development Officer, INITIAL Real Estate, Founder & Chief Possibilities Officer, ALIŌ – Building Wellbeing, Switzerland

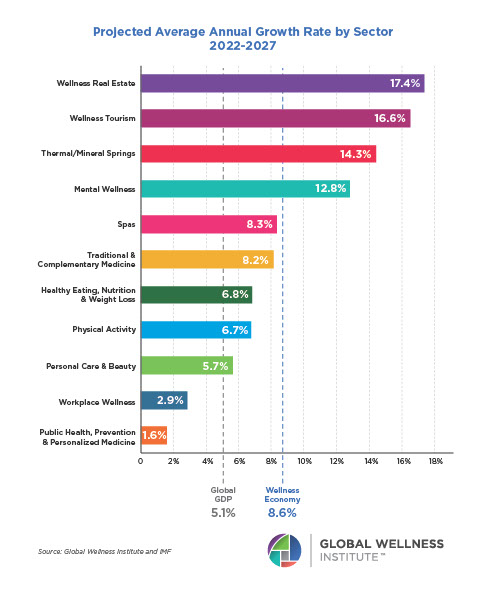

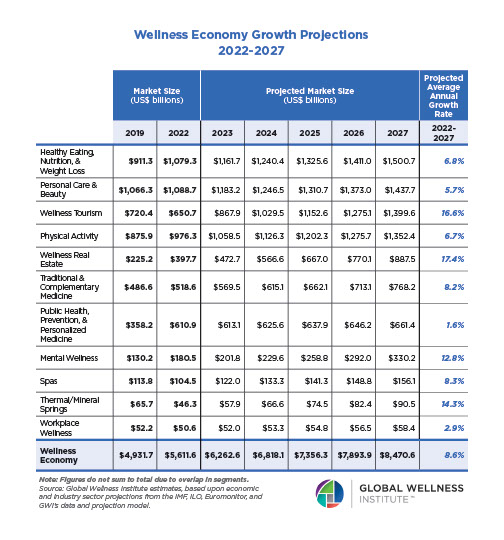

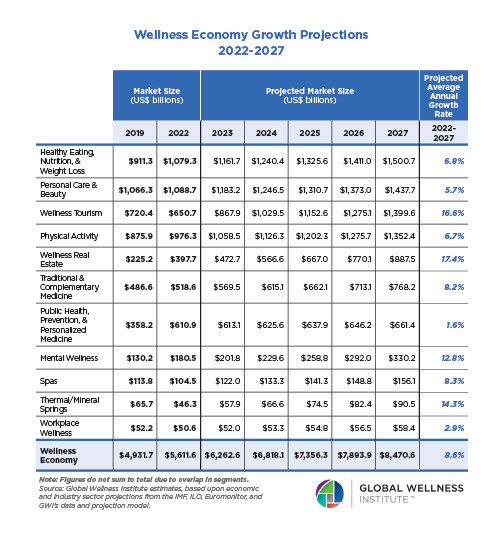

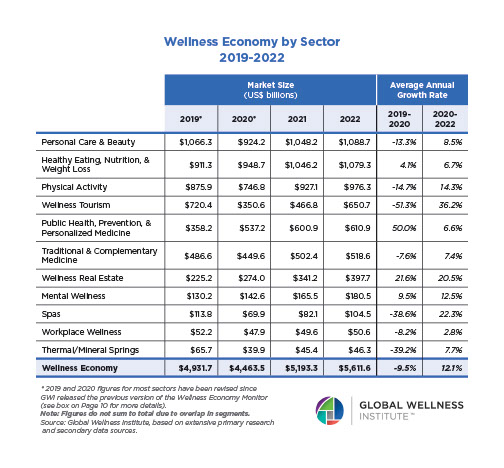

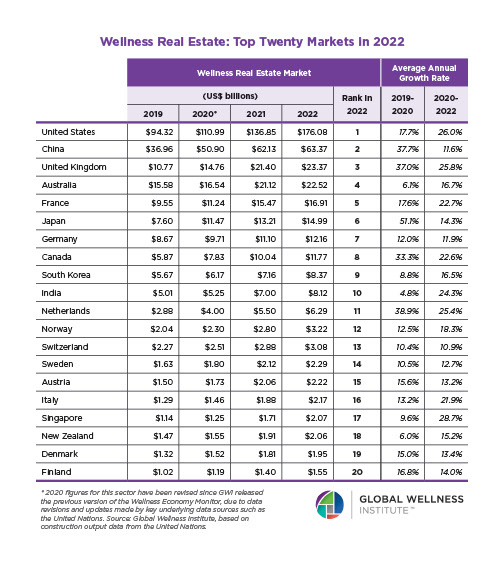

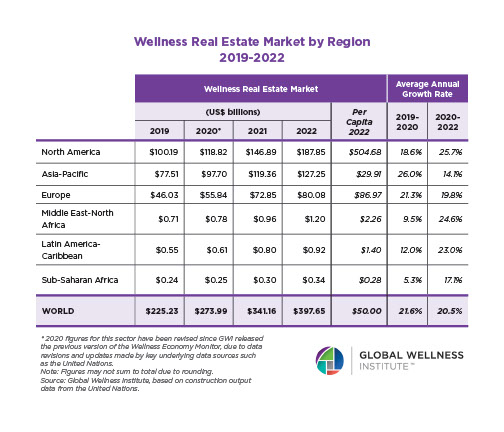

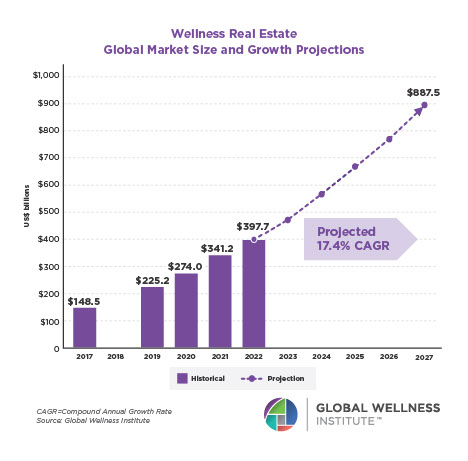

The wellness real estate sector, now valued at $548 billion globally and projected to reach over $1 trillion by 2029, is the fastest-growing sector in the wellness economy. In 2026, we are observing a market that is maturing—moving from aspiration to evidence, from luxury to broader accessibility, from building-centric design to community-scale thinking, and from amenity lists to integrated systems that actively support how people live, connect and age. This report identifies six trends shaping the next chapter of wellness real estate, each reflecting an observable shift already underway, supported by data, and creating real opportunities for developers, investors, designers and policymakers.

TREND 1: The Wellbeing Address – Where You Live Is How Long You Live

A fundamental shift is underway in what people expect from the places where they live, work and play. In the latest America at Home Study, 60% of all consumers cited health and wellness as the number one reason they desire certain home features, up 17% from two years prior. This is a market-wide demand signal reshaping how developers, designers and investors approach real estate at every scale.

Consumers are no longer satisfied with spaces that simply shelter. They want environments that actively support their health, wellbeing and longevity. A new category of development is emerging: communities and hospitality projects embedding preventive medicine, clinical partnerships and personalized health protocols directly into the real estate product. The home and the community are becoming points of care, not adjacent to healthcare, but structurally integrated with it. Healthspan is no longer adjacent to real estate. It is becoming infrastructure.

Wellness is now a foundational expectation influencing site selection, programming, spatial design and long-term operations. The built environment is not just a backdrop to life, but an active participant in how well and how long we live.

Resources:

- America at Home Study, consumer wellness priority data, 2025.

- Allen, J.G. & Macomber, J.D., Healthy Buildings, Harvard University Press, 2020.

- Global Wellness Summit, “Longevity Residences,” Future of Wellness 2026 Trends Report.

- National Association of Realtors, “Wellness Trend Driving Real Estate Price Premiums,” 2025.

TREND 2: Land First – When the Site Becomes the Strategy

A meaningful shift is taking place in how wellness real estate projects begin. Instead of acquiring a site and layering amenities onto a cleared parcel, a growing number of developers are starting with the land itself, its ecology, agricultural capacity, water systems and cultural assets, and designing real estate in response to it. The land is no longer a backdrop. It is becoming the framework.

Across asset classes, agriculture, biodiversity corridors, watershed systems and working landscapes are shaping site planning, phasing strategy and long-term value creation. The farm, vineyard or regenerative system comes first; real estate is designed around it. This is not farm-to-table branding. It is land-led master planning.

Consumer data supports the shift. Expedia’s Unpack 2026 report identified a 300% year-over-year increase in VRBO listings mentioning farm stays. The UN identifies rural and nature-based travel as one of the fastest-growing global tourism segments. US federal policy is also signaling alignment: the USDA’s $700 million Regenerative Pilot Program establishes soil health and land stewardship as national priorities with direct public health implications. Productive land systems diversify revenue through agriculture, hospitality, education and limited residential ownership, creating more resilient and differentiated development models.

Resources:

- Expedia Group, Unpack 2026 Travel Trends Report

- UN Tourism, Rural Tourism and Sustainable Development, 2024

- USDA, Regenerative Pilot Program, $700M federal investment, December 2025.

- Regenerative Farming as Climate Action, Journal of Environmental Management, 2023

TREND 3: The 3 Rs – Rest, Reset, Rejuvenate

Real estate designed for life balance

Something is shifting in what residents and buyers are telling the market they need. After years of optimizing for productivity, connectivity and performance, a counter-signal is emerging: people are seeking environments that actively support recovery, downtime and nervous system regulation as part of daily life. This is not a retreat from wellness. It is its maturation.

Gen Z and millennial buyers are increasingly prioritizing analog experiences, unplugging and in-person connection. Developers are responding with projects where rest and recovery are treated as programmable infrastructure—dedicated quiet zones, sensory-calibrated spaces for decompression, biophilic circulation paths, flexible micro-spaces for solitude and community programming built around restorative practices. The underlying insight is grounded in neuroscience—environments that support autonomic regulation and reduce sensory overload produce measurably better health outcomes and stronger emotional connection to place.

In an era of chronic overstimulation, the ability to offer genuine rest and recovery is becoming a competitive differentiator. Communities designed around life balance are seeing stronger resident engagement, and the rest ethic is emerging as a complement to the wellness features the market has already embraced.

Resources:

- The Design of Neighborhood Open Spaces to Improve Mental Health, Landscape and Urban Planning, 2024

- The Association of Resilience with Mental Health in a Large Population-Based Sample, International Journal of Environmental Research and Public Health, 2022

- Disconnect to Recharge: Wellbeing Benefits of Digital Disconnection in Daily Life, Communication Research, 2025

- Disconnected from complexity: on nature exposure, sociality, and the self-organizing self, New Ideas in Psychology, 2025

- Sax, David, The Future is Analog, PublicAffairs, 2022.

TREND 4: The Great Rebalance – Wellness Finds the Middle Market

Wellness real estate entered the market from the top. Most early projects have lived in the luxury segment. But an important shift is underway. The severe global housing supply gap, growing inequality and rising consumer demand for healthy homes at attainable price points are creating what may be the sector’s biggest unmet opportunity.

Early examples are emerging—master-planned communities demonstrating that wellness-centered design can be delivered at accessible price points without high-end amenity packages. Public-private partnerships and workforce housing developers are incorporating wellness principles like green space access, healthy building materials, walkability and social infrastructure into middle-market, affordable and rental projects. Housing is well established as a social determinant of health. National studies demonstrate that housing quality, stability and affordability directly affect health outcomes, and that renters face measurably higher health risks compared to homeowners.

Wellness design principles (walkability, biophilic elements, clean air, community connectivity) do not inherently require a luxury price tag. The developers and policymakers who figure out how to deliver wellness at scale and at price are positioned to impact wellness outcomes for all at a greater pace and scale.

Resources:

- Health Affairs, Housing and Health: An Overview of The Literature, 2020.

- American Journal of Public Health, Housing Status and Health in the United States, 2025.

- UnitedHealth Group, Affordable Housing Investments and Health Outcomes, 2025.

- Social Innovations Journal, Workforce Housing as a Population Health Strategy, 2025.

TREND 5: From Smart Homes to Sentient Neighborhoods

In 2025, we explored how AI-integrated homes are learning and adapting to their occupants’ needs. This concept is now scaling beyond the individual unit to the neighborhood and community level, increasingly powered by AI and informed by neuroscience.

Early adopters are deploying connected platforms that go beyond optimizing building systems, using data and AI to personalize community programming, facilitate social connectivity and activate shared wellness experiences. Community platforms are identifying which fitness classes, social gatherings or wellness resources residents engage with, and adapting offerings in real time. Neuroscience is also informing design—research confirms that light, acoustics, vegetation and spatial sequencing directly influence stress response, cognitive performance and emotional regulation. Environments with intuitive flow, circadian lighting, acoustic control and biophilic elements measurably reduce cognitive load. When combined with AI-driven community systems, the built environment moves from static infrastructure to a responsive, adaptive wellness platform.

Important questions around data governance, privacy and maintaining human connection are part of the emerging conversation. The next generation of wellness communities will not just be designed for wellbeing: it will learn and evolve with its residents.

Resources:

- PwC & Urban Land Institute, Emerging Trends in Real Estate, 2026.

- Terrapin Bright Green, The Economics of Biophilia, 2022.

- National Institutes of Health (NIH), research on neuroarchitecture and built environment stress response.

- Exploring the Role of Artificial Intelligence in Enhancing Social Participation for Community-Based Health Promotion: A Qualitative Study, Mass Gathering Medical Journal, 2025.

TREND 6: Designing Against Loneliness – Social Connection as a Design Brief

Something new is entering the developer’s design brief—the direct correlation between social infrastructure and human connection. The US Surgeon General’s 2023 advisory on loneliness and isolation spotlighted what researchers have documented for years—the built environment is an active agent in shaping, or preventing, social connection. This research is now influencing real estate design and programming decisions at the project level.

A growing number of master-planned communities are incorporating “social infrastructure” like front-porch architecture, third places designed for lingering, walkable layouts that create opportunities for casual encounter and intentional programming that give residents reasons to gather. A 2025 study in Health & Place confirms that well-maintained social infrastructure is a measurable factor in reducing loneliness. People with access to social infrastructure are three times more likely (32% vs. 9%) to say they have close friends. Gen Z and millennials are driving demand for spaces that foster belonging, not just shelter.

Developers are recognizing that social connection is not a soft amenity. It is a design decision with measurable impacts on resident satisfaction, tenant retention, community health and asset performance. The communities that intentionally design for belonging are differentiating themselves and becoming part of a solution to a broad social issue.

Resources:

- U.S. Surgeon General, Our Epidemic of Loneliness and Isolation, 2023.

- How the Neighbourhood-Built Environment Shapes Loneliness, Health & Place, Vol 97, 2026

- RE/Max Consumer Survey, Community and Social Connection Preferences, 2024.

- Survey Center on American Life, American Social Capital Survey, 2024.