By Susie Ellis, Chairman & CEO, the Global Wellness Institute

Last week I attended a medical tourism gathering in Tampa, Florida. One thing surprised me—and frustrated me at the same time. Many of the speakers—in fact, almost all of the speakers—said something along the lines of, “We don’t have reliable figures.”

Really? Still?

No figures on how much medical tourism is happening around the world? Can’t compare countries to countries? No agreed-upon definition of terms? No way to measure economic impact and opportunities?

It had been a while since I attended a medical tourism event, and I was aware many years ago there was an issue with lack of reliable data. But I thought that surely this would have been resolved by now. Well, apparently not and that is indeed unfortunate—for all of us. Lack of data and transparency results in misunderstandings, it slows down decision-making and definitely makes investment more risky. Odd, really, for a sector such as medicine that is all about precision and exactness. You would think there would be some good data available by now. But then I remember back to when my husband was in the hospital, and I was unable to get exact figures for the various tests and procedures on the bill. Should that tell me something?

I look at this in contrast to the world of wellness and wellness tourism in particular. I am happy to say we have some very good research data. As a result, my presentation on wellness tourism trends at this Tampa event featured slides filled with facts and figures. It is thanks to all of the research reports that were done by SRI International this past decade, and more recently by the Global Wellness Institute (GWI), as well as contributions from others like ISPA, that we can talk quite confidently and specifically about the world of wellness.

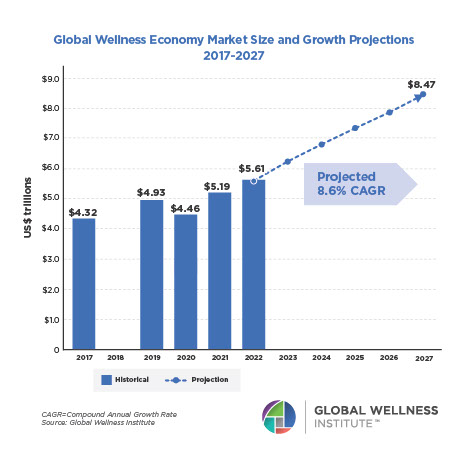

The GWI’s in-depth research reports on the wider, worldwide wellness market (2014) and the global wellness tourism economy (2013), the latest global research, give excellent data on the size of the wellness sector (now worth $3.4 trillion—or three times the size of the global pharmaceutical industry).

- This research divides the entire wellness market into 10 understandable segments: from fitness to workplace wellness.

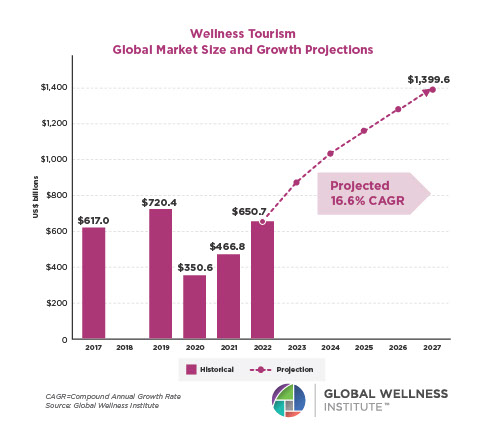

- The report estimates that wellness tourism is a $495 billion global industry,

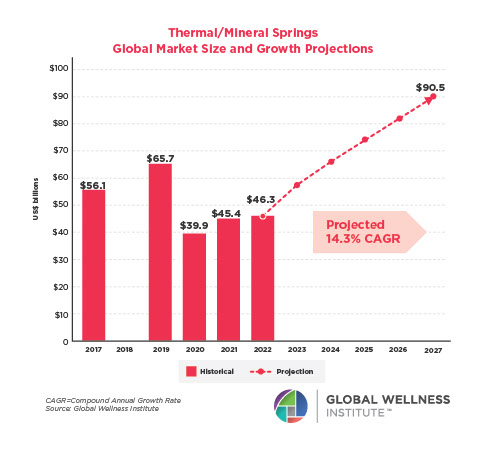

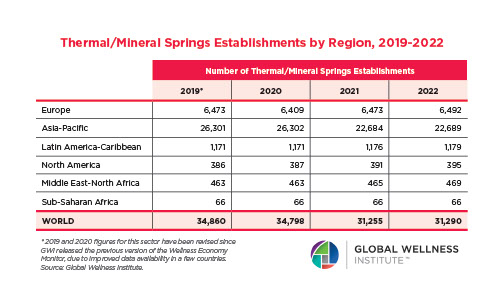

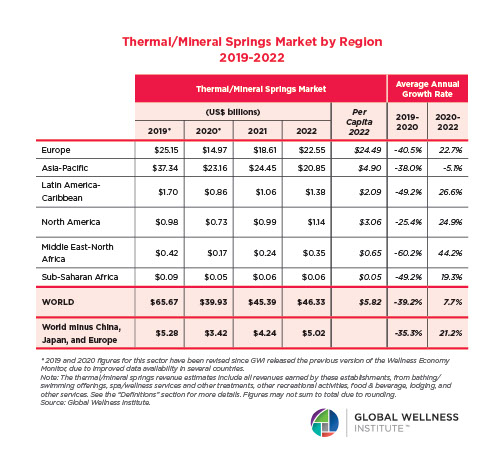

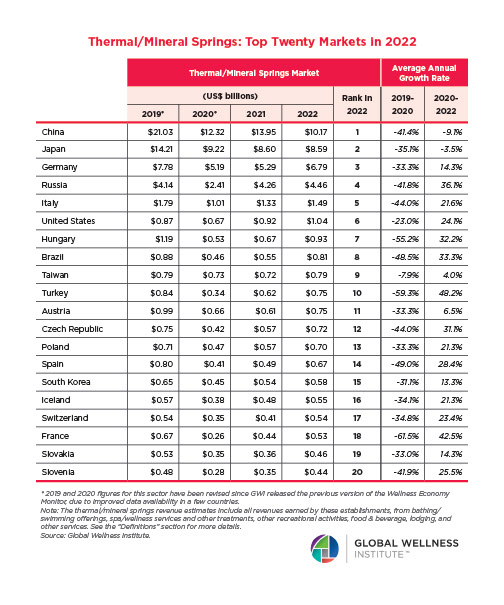

- It provided the first data on the number of thermal/mineral springs globally (26,847) – and by country!

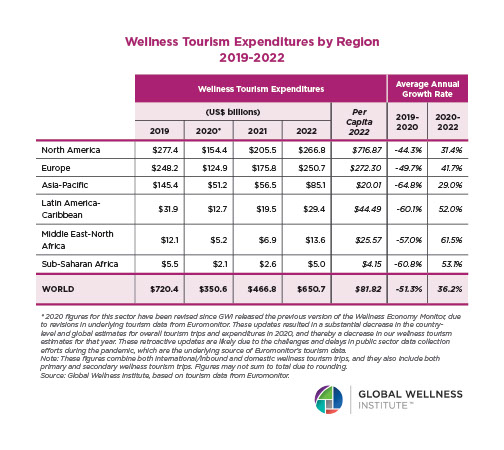

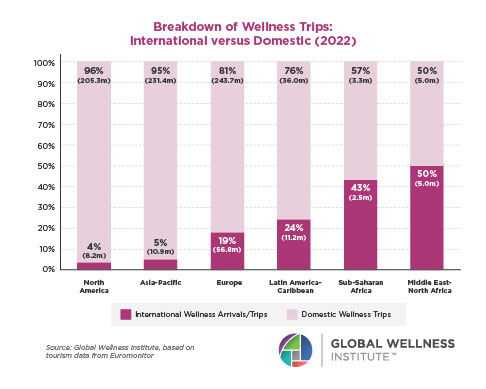

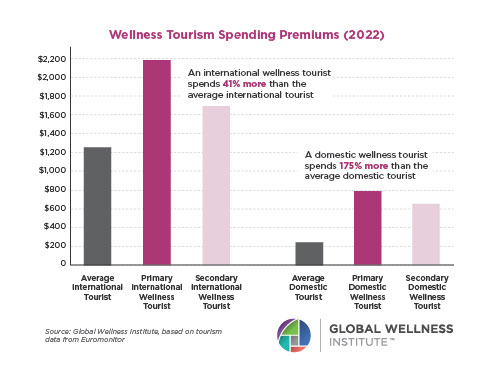

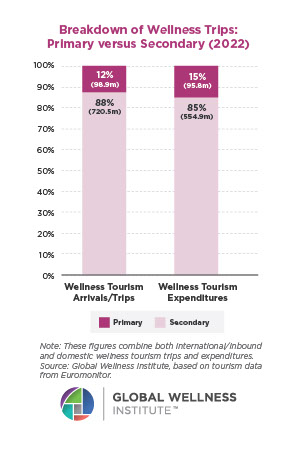

- It reports on the percentage of primary wellness travelers (13% of total trips, and 16% of expenditures) and secondary wellness travelers (87% of trips, and 84% of expenditures) – in addition to benchmarking the number of international (16%) and domestic (84%) wellness tourism trips taken annually worldwide.

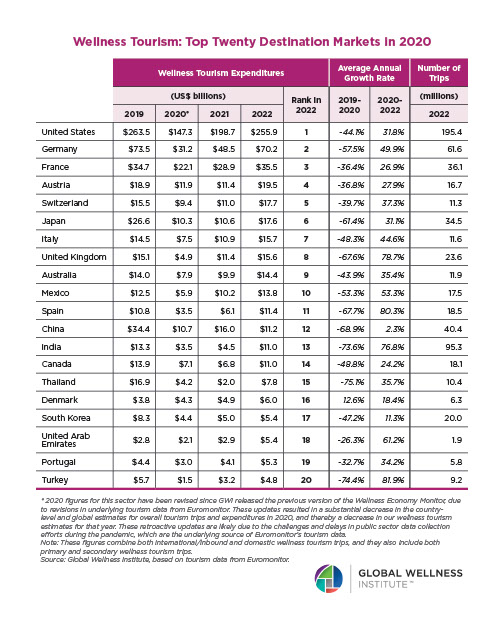

- And we can even compare one country’s annual data with another: for total wellness trips, inbound and domestic wellness trips, total expenditures, and even how much direct employment this travel category drives for that nation.

One reason I think this issue is front and center of my mind is because I am able to see our Global Wellness Institute in-house reports noting who has downloaded our research reports each day. The results have astounded me! Downloads from Ireland, Japan, Azerbaijan, India, U.S., Morocco, etc. – and that is just one afternoon! These are not made by just spa and wellness professionals, students and professors, but investors and even large consulting firms whose names everyone knows! We are indeed fortunate to have such valuable data in our industry—and we need to make sure we continue to invest in research data going forward.

I think it is worth pausing to celebrate what we—as a group—have accomplished. It has truly been a shared effort. The board of the Global Wellness Summit saw the need early on and commissioned the first global research report in 2007. Our research partner, SRI International, led by Katherine Johnston and Ophelia Yeung, turned out to be a great choice, and each of the seven research studies SRI has done for us resulted in groundbreaking numbers. Sponsors have stepped up each year to help cover costs (which are significant) of this global research so that we are able to make this valuable data available to anyone for free! Industry professionals have been generous with their time in taking surveys year after year and sharing data that helps our research become more and more accurate over time. I will even take a wee bit of credit for helping to define the research topics from one year to the next. In summary, it has been a collaborative effort and we all benefit as a result.

I am reminded there are other industries—travel and tourism, for example—that also have very good data. The World Travel and Tourism Council (WTTC) and the United Nations World Tourism Organization (UNWTO) have done a great job presenting research numbers year after year and making them available to the public. (My thanks to Jean-Claude Baumgarten, former chairman of the WTTC who now sits on our board, for having introduced us to these great resources.) Their spirit of collaboration has been similar to ours. In fact, when SRI did the wellness tourism research, they purposely aligned with the way the travel industry defines and reports tourism. After all, it helps all of us to be comparing apples to apples.

The medical tourism sector is at a place where it, too, would benefit greatly from getting global figures together. If I had just a bit more time (and someone would be willing to write a check to cover the expenses), I would be tempted to help shepherd the research so we would all benefit from reliable figures.

Just saying.

Agree wholeheartedly on lack of reliable data in the medical tourism sector. Divergent reports by established research houses such as Deloitte Health, spectacularly overs-forecasted US outbound medical travel at some 10 million patients in 2010, while McKinsey in the same month pegged the total number of international medical travelers at 65,000. Both reports were politically motivated, not data-driven, with an eye on the media, not objective research.

Similarly, and perhaps more unsettling in the data department, is the deplorable lack of consumer access to cost and clinical outcomes data for healthcare, including the full spectrum–from high-acuity tertiary care to the simplest preventive screening. Try to get a price for a simple MRI here in the US. Can’t do it. Try to learn about clinical outcomes for a hip surgery at Mayo vs. your local hospital. Nope, not available, not to healthcare consumers anyway. In an age of instant access to reliable information, the medical care industry status quo continues to keep patients in the dark, veiled in secrecy around patient protection, data privacy, and complexity-of-care hogwash. I look forward to the day when these walls come down and today’s healthcare druids become relics, artfully disrupted by technology and a good dose of healthy competition.