First-ever 15-Year Time Series Data for the Global Spa Industry—With Forecast through 2027

While the Global Wellness Institute (GWI) is well known for our comprehensive and rigorous wellness economy data, many may not know that our work began over 15 years ago with a focus on the spa industry. GWI’s lead economists released the very first global spa economy study in 2008. Since that time, our research has greatly expanded (alongside the growth of the Global Wellness Summit and the launch of the Global Wellness Institute) to encompass 11 diverse industry sectors that comprise the entire global wellness economy. In this month’s GWI brief, we are focusing on our long-term data collection efforts for the spa industry, including the first-ever snapshot of our full time-series dataset from 2007 to 2022, and projecting forward to 2027.

How do we collect spa industry data?

Even though the spa industry is one of the smallest sectors of the wellness economy, GWI’s work to estimate its global and country-level figures takes the longest of all 11 sectors! Compiling spa industry data is a complex process taking several months to complete every time we release new figures. Our methodology is multifaceted, measuring seven categories of spas, and each category requiring a separate data collection method.

For destination spas and health resorts, thermal/mineral springs spas, and cruise ship spas, we use a very granular, “bottom-up” approach. There is no econometric model to estimate these segments because they are based on unique historical, cultural, natural, and socioeconomic features in each country. Since 2008, GWI’s research team has compiled massive databases that count the destination spas/health resorts, thermal/mineral springs spas, and cruise ship spas located in 218 countries and territories. While we can never be sure that our database is 100% exhaustive (every year we track new openings and discover smaller properties that we had previously “missed”), we are confident that the thoroughness of our databases provides a strong basis for making accurate estimates for these spa segments in each country.

Other spa categories—including day/club/salon spas, hotel/resort spas, medical spas, and “special” country-specific spa segments—are far too large in many countries for us to compile a global database or count properties. For these categories, our methodology depends on the type of country:

In larger countries (approximately one-third to one-quarter of the countries we cover), we have developed an econometric model to help us make estimates for each spa segment, based on a wide variety of input factors, like population, income level, tourism sector development, etc. The model also takes into consideration our team’s extensive research on spa/wellness market history and development in each country. And we also rely upon interviews with spa industry leaders working in these regions, as well as information from industry associations or government datasets, where available.

In smaller countries (at a low/middle-income level, and/or with very small or developing spa markets), we continue to maintain a database and “count” spas for day/club/salon, hotel/resort, and other spa categories. These numbers are based on a wide variety of sources, including tourism websites and booking engines, regional industry associations, and Google business listings.

Since 2008, our research has benefitted immensely from the deep global experience of dozens of GWI stakeholders working in the spa industry all around the world. These partners have supported our work in many ways, including sharing regional and country-level industry insights, conducting industry surveys, helping us to access foreign language government and industry association datasets, and even sharing revenue information for their own businesses.

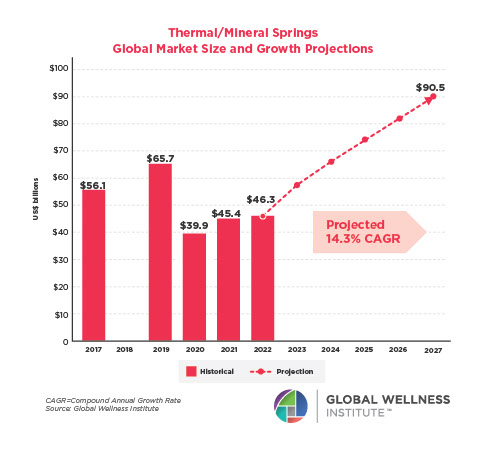

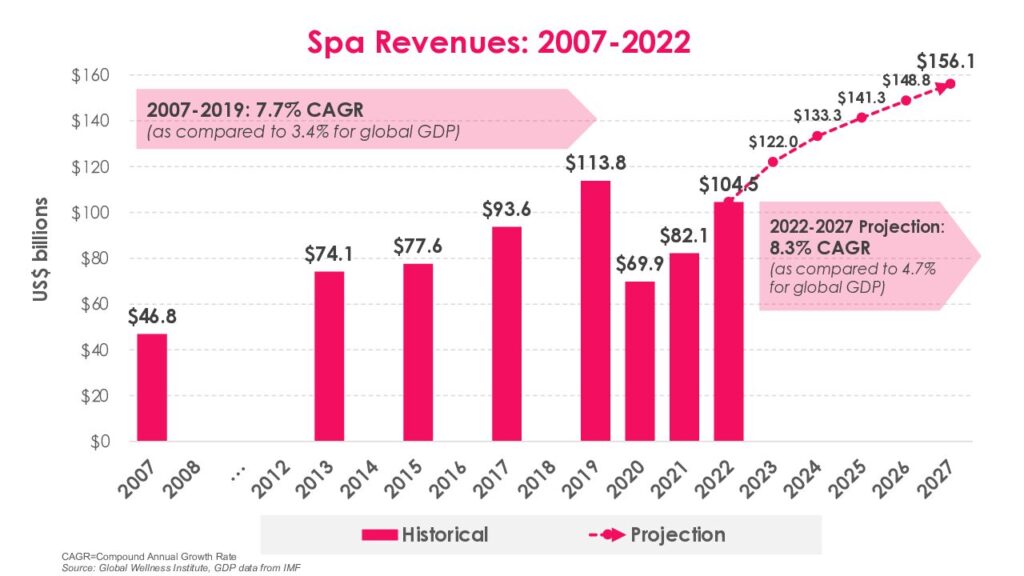

The spa industry was hit hard by the pandemic, but its longer-term growth trajectory is robust.

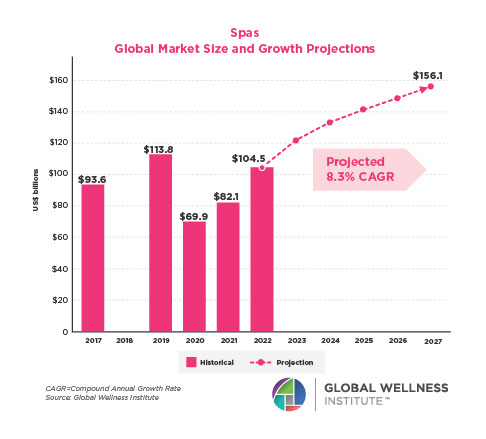

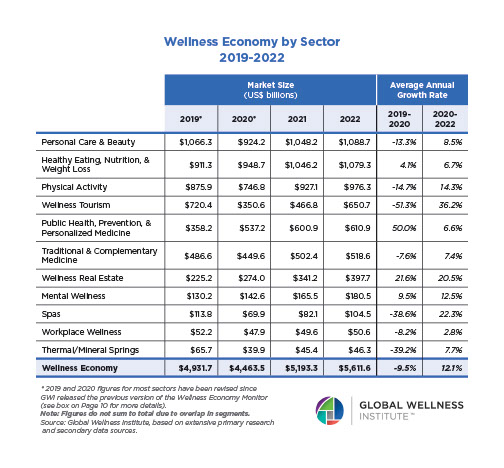

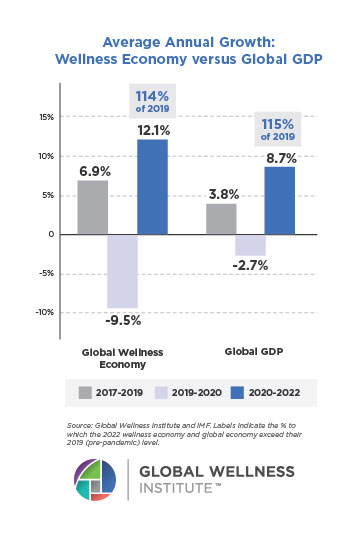

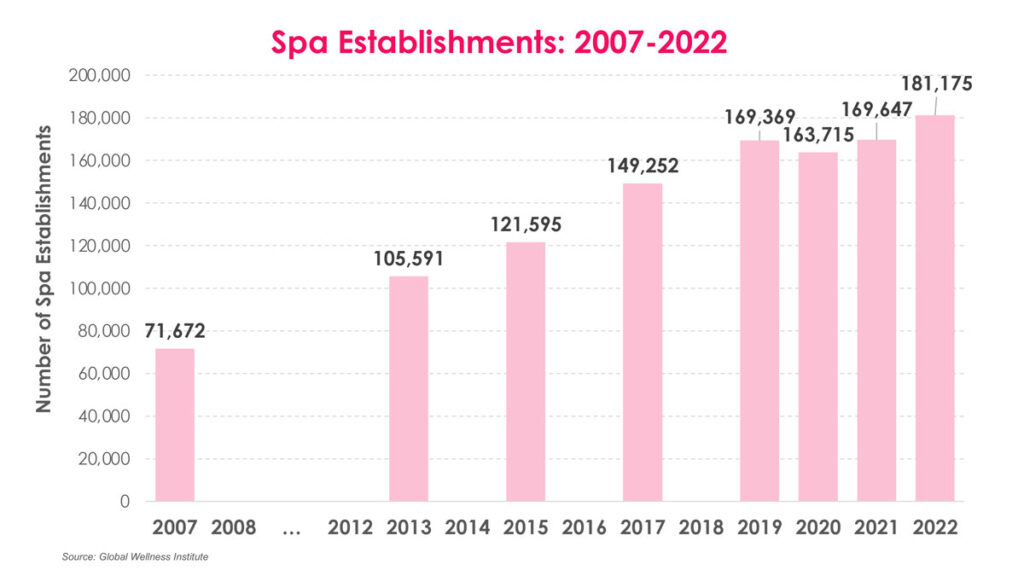

Prior to the pandemic, spa industry revenues were growing at a robust rate of 7.7% annually (2007-2019), which is more than double the rate of global GDP growth during this time period. The number of spa establishments also grew at an astonishing rate during this period, with the number of spas operating around the world expanding by 2.3 times from 2007 to 2019.

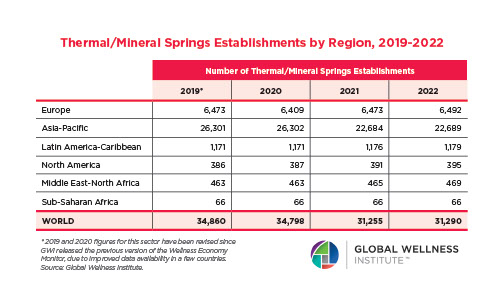

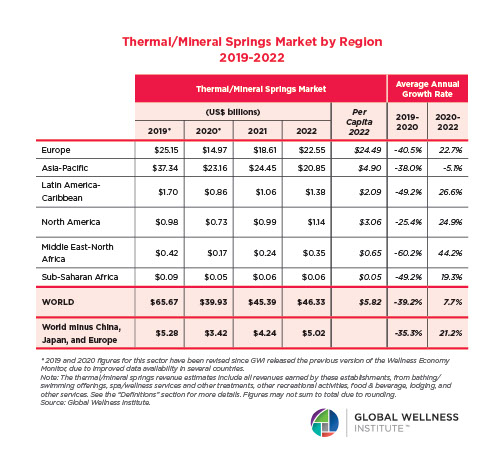

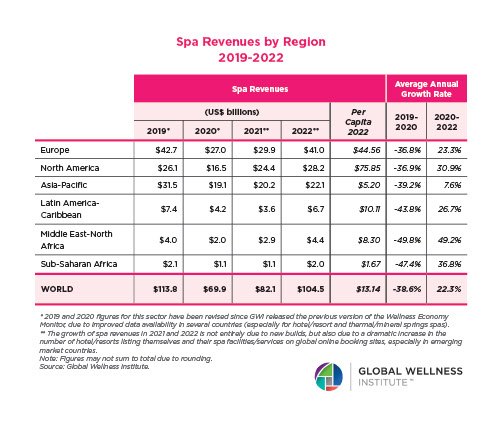

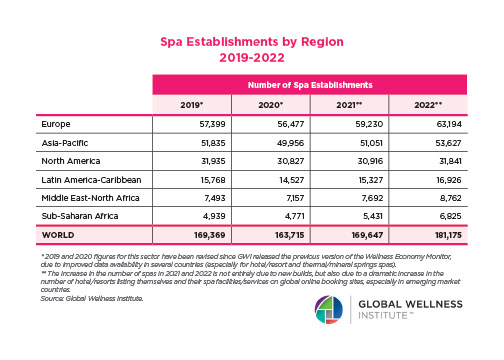

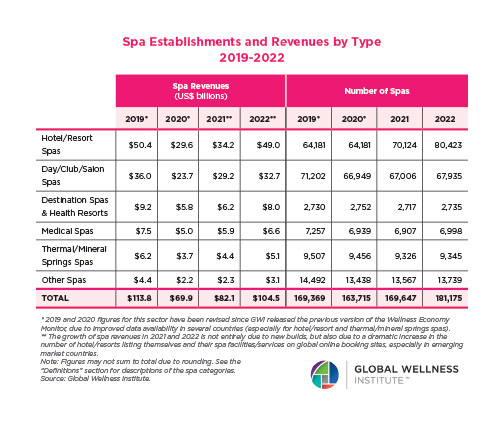

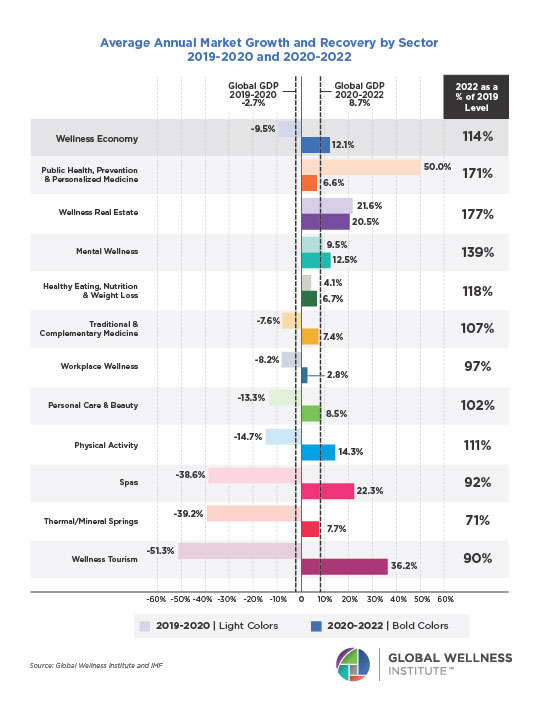

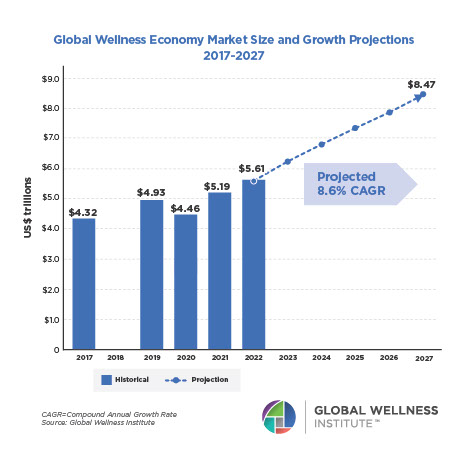

Because many types of spas are tourism-dependent businesses, the sector took a strong hit from the border closures, travel bans, business shutdowns, and capacity restrictions during the pandemic. Spa revenues fell by 39% globally in 2020, while the number of spa establishments fell by more than 5,600. Spa revenues have slowly come back in 2021 and 2022 (but were still slightly below their pre-pandemic peak of $113.8 billion). Spa establishment openings recovered more quickly, and as of 2022, the number of spa businesses reached a new peak (181,175 spas across 217 countries) that far exceeds its pre-pandemic level.

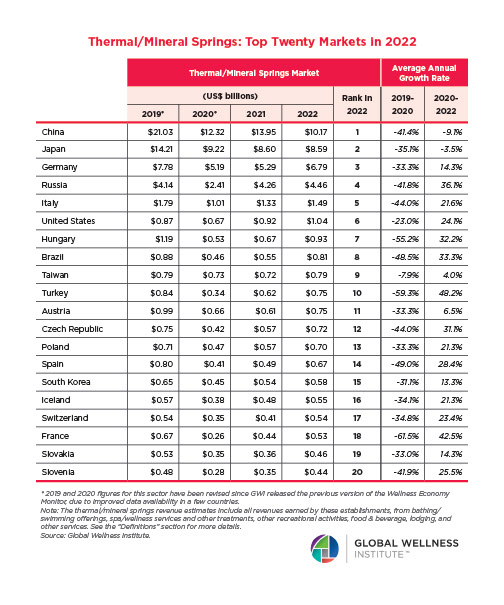

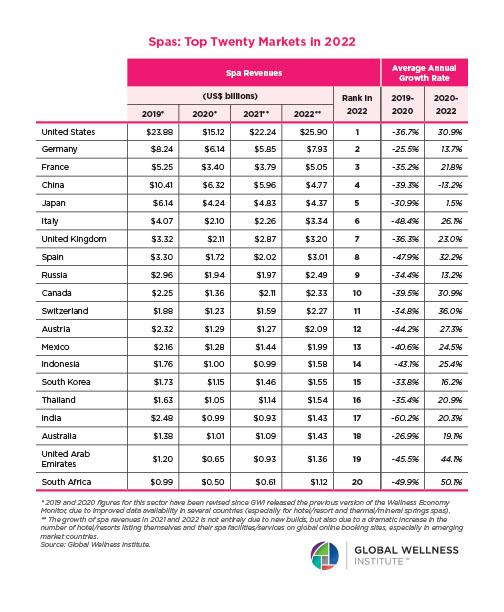

As of the end of 2022, approximately 86 countries had spa industry revenues that had recovered to, or surpassed, their pre-pandemic levels, including the United States, Canada, Switzerland, Australia, and United Arab Emirates. About 131 countries had not fully recovered by the end of 2022 (most were at 80-99% of their pre-pandemic levels).

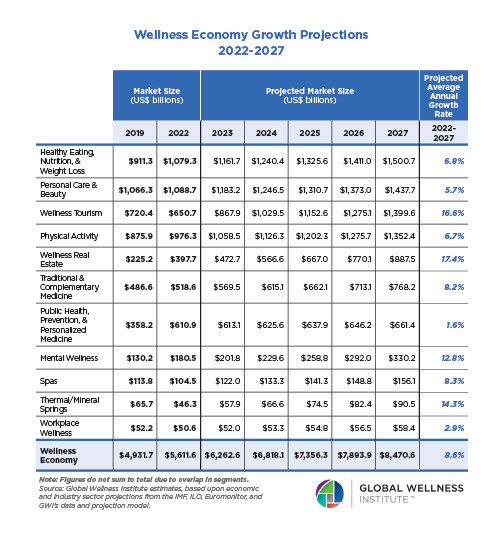

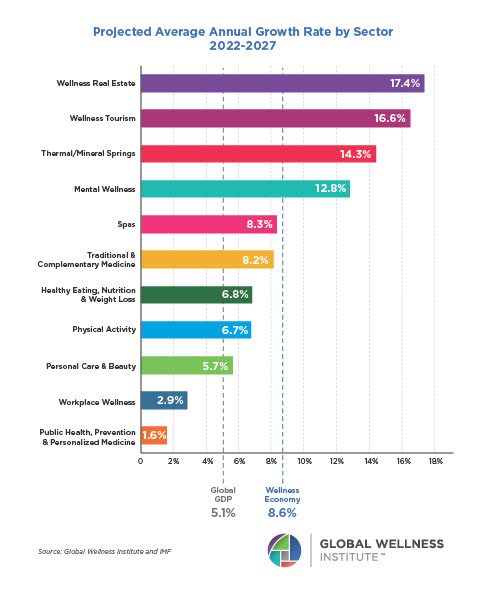

With a projected annual growth rate of 8.3% from 2022 to 2027, we expect that the spa industry will fully recover and exceed its pre-pandemic level in 2023. Note that these projections were made in the fall of 2023, and they will be updated with the release of the next Global Wellness Economy Monitor in the fall of 2024.

For more data on the spa industry, see the most recent edition of GWI’s Global Wellness Economy Monitor.