Technology is arguably the biggest force driving change in the physical activity economy, bringing new business models and methods of participation, new ways to reach customers, and new kinds of devices and equipment. Technology is transforming how consumers engage with all types of fitness and physical activity, enabling us to track our own metrics, monitor performance and progress, access programs and services on demand, and connect with like-minded “tribes” and communities.

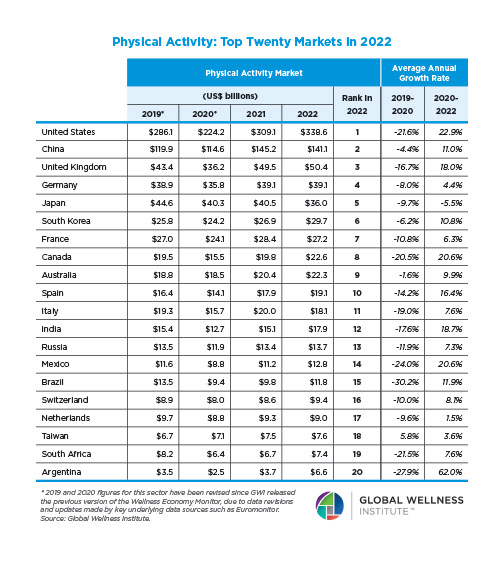

GWI estimates that technologies related to recreational physical activity represented a $26.3 billion global market in 2018. Asia-Pacific is the largest regional market, at $10.8 billion, because it is the world’s largest consumer market for fitness wearables and trackers. North America ranks second in size for technology, at $8.6 billion, and it is the largest region for technology services that support physical activity (e.g., streaming services, apps, intermediaries, software, and other platforms). The United States and China are the dominant countries in the physical activity technology sector, accounting for over half the market in 2018. The GWI report, Move to be Well: The Global Economy of Physical Activity, further breaks out the market sizes for this segment across the world’s regions and the top 20 countries.

The physical activity technology landscape encompasses a diverse range of devices/equipment and software/services (as elaborated in the table above) that support people’s participation in fitness, sports, active recreation, and mindful movement in many different ways. With promises of making exercise more convenient, fun, affordable, personalized, portable, social, gamified, trackable, efficient, and results-oriented, these technologies are seeing a rapid uptake by consumers all over the world, even in countries that have not previously had well-developed fitness and gym offerings.

On the other hand, all of these technologies are so new that there is not yet conclusive scientific evidence on what is effective at changing behavior and increasing physical activity and what is just a gimmick. The rise of fitness and health tracking, monitoring, and connectivity is also giving rise to a host of concerns related to personal security and privacy, stress and anxiety, the impacts of digital versus face-to-face connections, and other issues. While trackers, apps, social media platforms, streaming services, etc., may be adding a level of convenience, motivation, and fun to exercise, it is also important to keep in mind that these technologies are not essential for people to be physically active. Hundreds of thousands of people around the world get enough movement each day with nothing more than a pair of shoes, a simple bicycle, or a ball and an empty field. In many ways, technologies are attempting to fill gaps in our built environments and lifestyles that prevent us from getting enough movement. As long as our environment continues to favor a sedentary lifestyle over movement and our busy lives keep us from exercising, we will be looking to technology to help reduce those barriers.

The Diverse Landscape of Physical Activity Technologies

Streaming and on-demand services: While at-home and on-demand fitness first emerged in the 1980s (the early years of video technology, the fitness boom, and Jane Fonda VHS tapes), today’s technology-driven streaming and on-demand exercise options have become a major disruptor in the industry. GWI estimates that online and app-based streaming/ on-demand exercise classes and workouts were a $6.1 billion market globally in 2018 (this represents about 4.4% of global consumer spending on doing fitness and mindful movement activities). The range of options span every category of exercise imaginable (spin, running, boxing, dance cardio, yoga, barre, ballet, and so on). They include: subscription, pay-as-you- go, and free options; live-streamed and on-demand/recorded classes; equipment-linked services (e.g., Peloton, Mirror); gym/studio spin-offs (e.g., Exhale On Demand); celebrity/ influencer-based workouts (e.g., AKT On Demand, TA Online Studio); online-only services (e.g., Daily Burn, Keep); and virtual personal training (e.g., Aaptiv Coach). Most streaming/ on-demand services are currently U.S.-based, although China and the United Kingdom are also rapidly-growing hubs.

Apps: The first fitness apps were launched in 2008, soon after the introduction of the iPhone and the Apple App Store. There are now an estimated 250,000-300,000+ fitness and health apps available for download, generating an estimated $2.4 billion in user revenues in 2018 (from downloads, upgrades, and in-app purchases). Most fitness apps focus on tracking, measuring, and analyzing various fitness and health metrics (e.g., tracking workouts, counting steps, monitoring fitness goals, counting calories consumed and burned, etc.). Some of the most popular apps in this category are free for users (e.g., My Fitness Pal, Samsung Health, Pacer), although many are paid or offer a premium/paid upgrade option. Apps are increasingly adding a social and community dimension (e.g., Runtastic, Joyrun), or an element of gamification, competition, and rewards (e.g., Fitocracy, Yodo Run, Nexercise). Some include informational/educational tutorials, while some provide personalized music and playlists for workouts (e.g., RockMyRun, Fit Radio). Some popular apps are connected with wearable devices (e.g., Fitbit, Codoon), and some are connected with major fitness brands (e.g., Nike Run Club, UA Record). (Note that GWI has separated apps that focus primarily on providing streaming/on-demand workouts and classes into a separate category, above.)

Software and platforms: Estimated at $1.4 billion globally in 2018, a wide variety of software and online services and platforms are streamlining management, booking, and customer- facing functions across all types of physical activity-related businesses. The emergence of class finder and booking intermediaries has been a major disruptor for gyms and fitness studios in the last five years – ClassPass is the largest player, although there are many other competitors across different regions, such as Singapore-based GuavaPass (recently acquired by ClassPass), UK-based PayAsUGym, Gympass (focused on the corporate market), India- based FitPass, FitReserve, and others. The other major segment in this sector is booking, scheduling, billing, and back-office management software and systems. Mindbody is the most recognized player in this segment, but there are dozens of other services focusing on different types of businesses, such as gyms (e.g., Virtuagym), sports and active recreation providers and nonprofits (e.g., ACTIVE Network, PerfectMind), yoga studios (e.g., TULA), dance studios (e.g., The Studio Director), martial arts (e.g., Kicksite), personal trainers (e.g., My PT Hub), and so on. The United States is home to the largest number of exercise- related software services and platforms, although other countries that have sizable tech and software industries also have many companies and start-ups (United Kingdom, Canada, India, China).

Wearables and trackers: At $14.7 billion in 2018, wearables represent over half the technology market. This category includes fitness bands (e.g., Fitbit, Garmin, Polar, Huawei Band, Xiaomi Mi Band) and other types of activity trackers that range from simple pedometers to high-tech clip-ons. Other types of sensor-embedded trackers and fitness wearables have emerged in recent years including smart jewelry (e.g., Bellabeat Leaf, Misfit Shine); smart clothing (e.g., Hexoskin, Sensoria fitness socks, Nadi X yoga pants, SUPA Powered sports bra); smart footwear (e.g., UA HOVR shoes, Altra IQ shoes, Digitsoles, Lechal smart insoles); and smart eyewear (e.g., Recon Jet, Vue, Level, Solos AR smart glasses).

Smart and networked equipment: Estimated at $1.7 billion in 2018, exercise/fitness/gym equipment and sporting goods embedded with sensors and networking capabilities are a small but rapidly growing portion of the fitness/sports equipment and supplies market. This category includes sophisticated fitness and gym equipment with connectivity, tracking, streaming, artificial reality, and other high-tech functions (e.g., treadmills, ellipticals, stationary bikes, other cardio/strength training equipment). All types of sporting goods and equipment –balls, bats, tennis racquets, golf clubs, etc. – are also being transformed by sensors and smart functions that track metrics, analyze performance, provide virtual coaching, and much more.

Exergaming: The video gaming industry made its first foray into fitness in the 1980s with early versions of virtual reality exercise systems (e.g., HighCyclevirtual exercise bike and Atari Puffer game-connected bike) and fitness mats connected with gaming systems (e.g., Nintendo Power Pad and Atari Foot Craz). While none of these early products were successful, the “exergaming” or “exertainment” industry started to take off with the launch of the Dance Dance Revolution game in 1998, the Wii Fit system in 2007, and the advanced Kinect motion detection in 2010 (allowing a person’s body to become the game controller). The proliferation of mobile devices and gaming apps in the last decade has brought wildly popular augmented reality exergaming apps like Zombies, Run!; Pokémon GO; and Superhero Workout. Today, every major gaming system offers a wide array of fitness-focused games and connected controllers/equipment, such as Wii Sports, EA Sports Active 2, Nike+ Kinect Training, Just Dance, etc. GWI has not estimated the market size for exergaming because no recent data are available, and it is not possible to separate fitness-focused games and gaming equipment (hardware/controllers) from the overall video gaming, eSports, and related markets. A ten-year-old study by the U.S.-based Games for Health Project found that worldwide sales of health-focused games (e.g., Wii Fit, EA Sports Active, Dance Dance Revolution) totaled $2 billion over an 18-month period in 2009.41

41 Brice, K. (2009, June 26). Health games notch up worldwide sales of over $2 billion – report. gamesndustry.biz. https://www.gamesindustry.biz/articles/health-games-notch-up-worldwide-sales-of-over-USD2-billion-report.